Copay and Coinsurance

Copay and coinsurance are two types of costs you have to pay for health care services.

Copay vs. Coinsurance

What's the difference?

Both terms are what insurance companies refer to as cost sharing. More simply, the share of medical expenses that you are expected to pay.

A copayment is a specific dollar amount you are usually asked to pay at the time you receive healthcare services. An office visit to the family doctor will have a copay.

A coinsurance is a percentage of the allowed charges. Coinsurance is almost always much higher than a copay.

Copay

This is a fixed amount you pay for a covered health care service, usually you are asked to pay this when you get the service.

The amount can vary by the type of covered health care service.

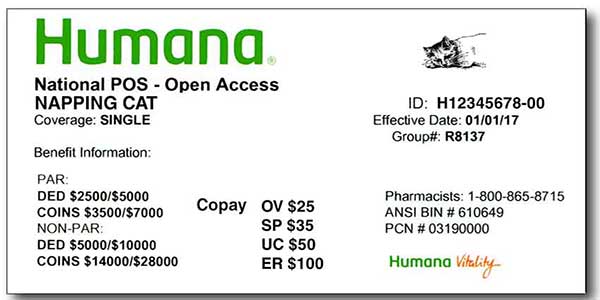

The copay amount will be listed on your insurance card. Depending upon your plan it may read:

| Service | Copay |

|---|---|

| Office Visit (OV) | $25 |

| Specialist Office Visit (SP OV) | $35 |

| Urgent Cae (UC) | $50 |

| Emergency Room (ER) | $100 |

You will also have a copay when you get a prescription filled.

Generic drugs have the lowest copay and non-preferred brand drugs the highest copay.

♦ One of the results of the Affordable Care Act was that after 2014 copays count toward the out-of-pocket maximum.

However, they do not have to count toward the deductible.

• There are a few plans that count copay toward meeting the deductible but they are the exception.

Consult either your plan’s benefits description or call the customer service number on your insurance card to be sure.

• Some plans limit the number office visits or treatments at a specific copay. After that number is reached, these plans usually apply the charges to the deductible.

This can become costly if you need more visits than the plan allows.

• This limitation also discourages people from seeking care when they should because they are afraid of exceeding their limit.

Fortunately, most health plans must now cover a set of preventive services — like shots, physical exams and screening tests — at no cost to you.

This includes plans available through the Health Insurance Marketplace.

♦ For some services, you may have both a copay and coinsurance.

Example

You visit to a pulmonologist (lung specialist).

You will have a charge for a specialist office visit, copay.

You could have a separate charge for any breathing tests they give you since these are not preventive.

♦ The charges you will receive depends upon how the bill is submitted to the insurance company and also the contract your plan has with providers.

Unfortunately, you will not find this out until you receive an Explanation of Benefits (EOB).

♦ When choosing a new plan you need to think about how often you visit a doctor or take expensive drugs, you might want to choose a plan that has a low copay.

Coinsurance

Coinsurance is usually a percentage of the allowed charges (for example, 20%).

• You pay the percentage after first paying your deductible.

This should not be confused with the term copayment.

• Copayment is a fixed amount (for example, $25 for an office visit).

Health insurance plans vary greatly in how and for what kind of services to require a coinsurance so you need to read your plan’s documents carefully.

Plans with both in-network and out-of-network benefits usually have a lower coinsurance percentage for in-network providers than those out-of-network.

It is common to have a 20 – 30% coinsurance.

Example

• Your insurance allowed $1,000 for a special test and you have already met your deductible, your coinsurance payment of 20% would be $200.

• Your insurance would pay the rest of the allowed amount, $800.

Keep in mind, the amounts you pay as a coinsurance count toward reaching your out-of-pocket maximum.

♦ Once your reach your plan’s out-of-pocket maximum you stop paying a coinsurance and the plan then pays 100%.

When you choose a health insurance plan, it’s important to understand what your insurance company covers and what they require you to pay as coinsurance.

As a rule, the lower the coinsurance percentage the higher the plan’s monthly premium.

♦ If you apply through the Marketplace you may qualify for Cost-Sharing Reduction (CSR).

With CSR you can save money by receiving a lower premium, lower copay, lower coinsurance and lower deductible.

♦ It is important see if you qualify for CSR.

Cost-Sharing Reductions is sometimes confused with the term Out-of-Pocket Savings.

If you qualify for Cost-Sharing Reductions you will receive Out-of-Pocket Savings. Thank our elected officials for cooked up these phrases.

Read how Out-of-Pocket Savings and Cost-Sharing Reductions can work for you.